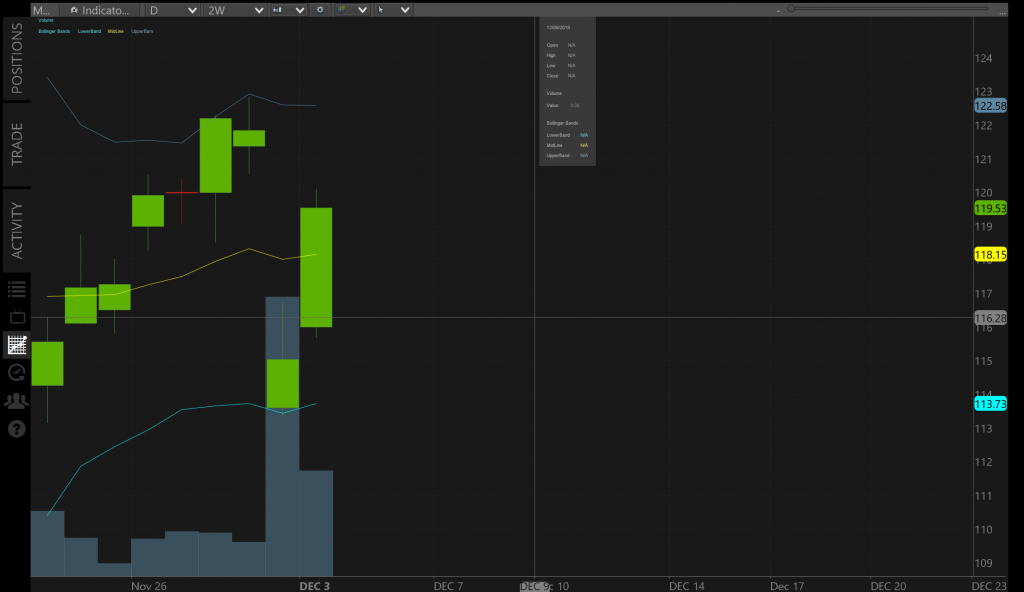

The next company that is allegedly going out of business from hackers has been discovered. $ANTM supposedly had around 80M records taken. If only they were filming a movie about North Korea at the same time. We can see that amid all the panic that the professionals were moving into the stock.

The first observation is that the stock hits a high for the week on the news and stays above the current upward trend. The next day it rockets straight up at market open. Lets also take a look at Time & Sales on the right side of the screen. Lots of red means than there are sellers. But buried among the haystack are two interesting needles. Someone bought 30,000 shares of $ANTM. You’re not going to plow $4,110,527 into a stock that is going out of business. But wait! There’s more!

At market close someone bought 59,894 shares. You’re not going to plow $8,219,253.62 into a stock that is going out of business. Anytime you see a big buyer move in you know there’s some confidence in the underlying.

We can see that the options market is hot on the news. IV is around 27%, which is relatively low. The IV Percentile is around 44% which isn’t high enough to warrant shorting volatility. You would want to see that number above 50% to make it worth your while. When we look at the Puts there is a 31.59% chance that the stock will be below $130 at options expiration 35 days from now.

All signs are pointing to calculated buying and minor impact, unless the cold weather returns.